Is there a case for Cambo, Rosebank or Glendronach?

SHETLAND-based Daniel Gear works on some of the “technical and practical” aspects of the energy transition towards net zero.

In this Viewpoint contribution Gear – who has a role at new locally based engineering group Voar Energy – reflects on potential oil and gas developments around Shetland, such as the controversial Cambo field, in a UK that is exposed to extreme price volatility further heightened by the tensions with Russia.

Over the space of a few short years, we have observed the engines of industry overcome the inertia of three centuries of climate indifference, and steadily build momentum toward the transformation of our energy systems.

In the West, particularly in the UK, this momentum now feels virtually unstoppable, and most of us can agree – if not on the route – that we should at least strive for a common destination whereby harmful emissions have been eliminated from our way of life.

We know that such a transition isn’t straightforward; we should be prepared for increasingly shuddering collisions as our seemingly unstoppable energy transition crosses orbits with our demonstrably immovable energy markets. The effects of one such glancing collision is playing out now, as energy prices hit stratospheric levels across Europe, driven in a large part by demand for natural gas and the associated risk to supply due to tensions with Russia.

The cost of this collision exacerbates societal issues that are closer to home; Ofgem’s eye-watering 54 per cent energy price cap hike will inevitably act to compound the already high rates of fuel poverty in Shetland.

Another fragment from an earlier orbital collision is the development of the Cambo field, West of Shetland, which would produce around 50,000 barrels per day (bpd) and 30 million standard cubic feet (scf) of gas per day during phase one of its development.

Become a member of Shetland News

The intuitive response to Cambo, is that the development is clearly incompatible with the energy transition and Scotland’s climate commitment.

Rosebank would appear to fall into a similar category, with peak production forecast at 92,000 bpd and 74 million scf of gas per day, while the huge Glendronach gas development – comprising around 600 billion scf of gas – seems set to move ahead following TotalEnergies confirmation of investment into a mercury removal unit for the treatment of such gas.

But like sensitivities in an economic model that unexpectedly invert the whole outcome, Cambo, Rosebank and Glendronach are deserving of a closer look, particularly from those who support the lowest carbon transition possible. To understand why, we need to look at how the UK and European energy markets work.

UK gas supply

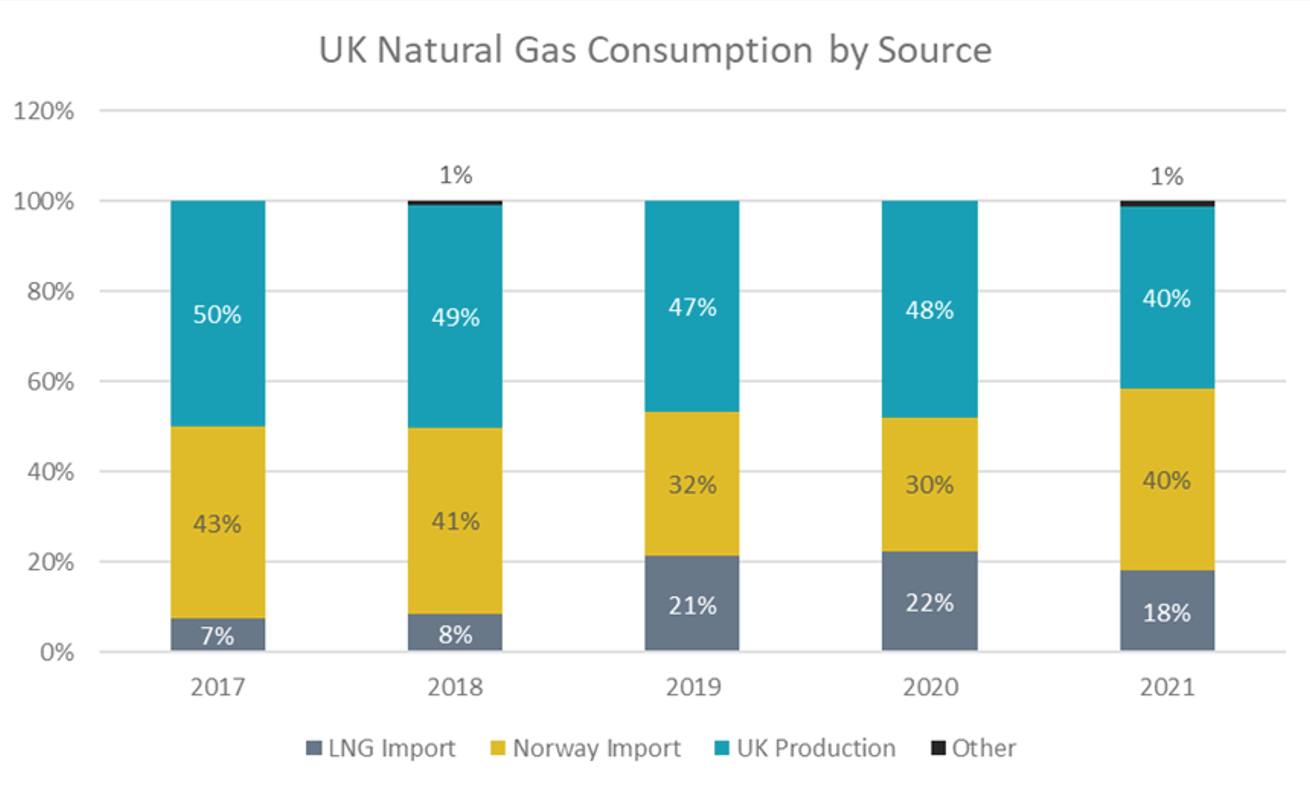

In the UK, 85 per cent of homes are heated by natural gas. Within the National Grid over the past year, 40 per cent of electricity was generated using gas turbine generators. To quantify how much gas this represents, annual UK demand has consistently been around 80 bcm over the past five years, with the exception of 2020, which was around five per cent lower due to effects of the pandemic.

Norway is the largest external supplier of gas to the UK, and the second largest supplier to the rest of Europe after Russia. Like the UK’s own production, Norway’s exports are not limited by infrastructure constraints, rather the limitation is on how much they can produce.

With Norway also being the second largest supplier to Europe, the only way that more gas could be supplied to the UK would be if exports were diverted from one of their other major export pipeline destinations in Germany, France, Belgium or the Netherlands.

The UK’s failure to invest in gas storage infrastructure is also relevant. Continental Europe has storage capacity available for 22 per cent of their total annual demand, while the UK can store just one per cent of annual demand (or roughly four days’ worth of gas).

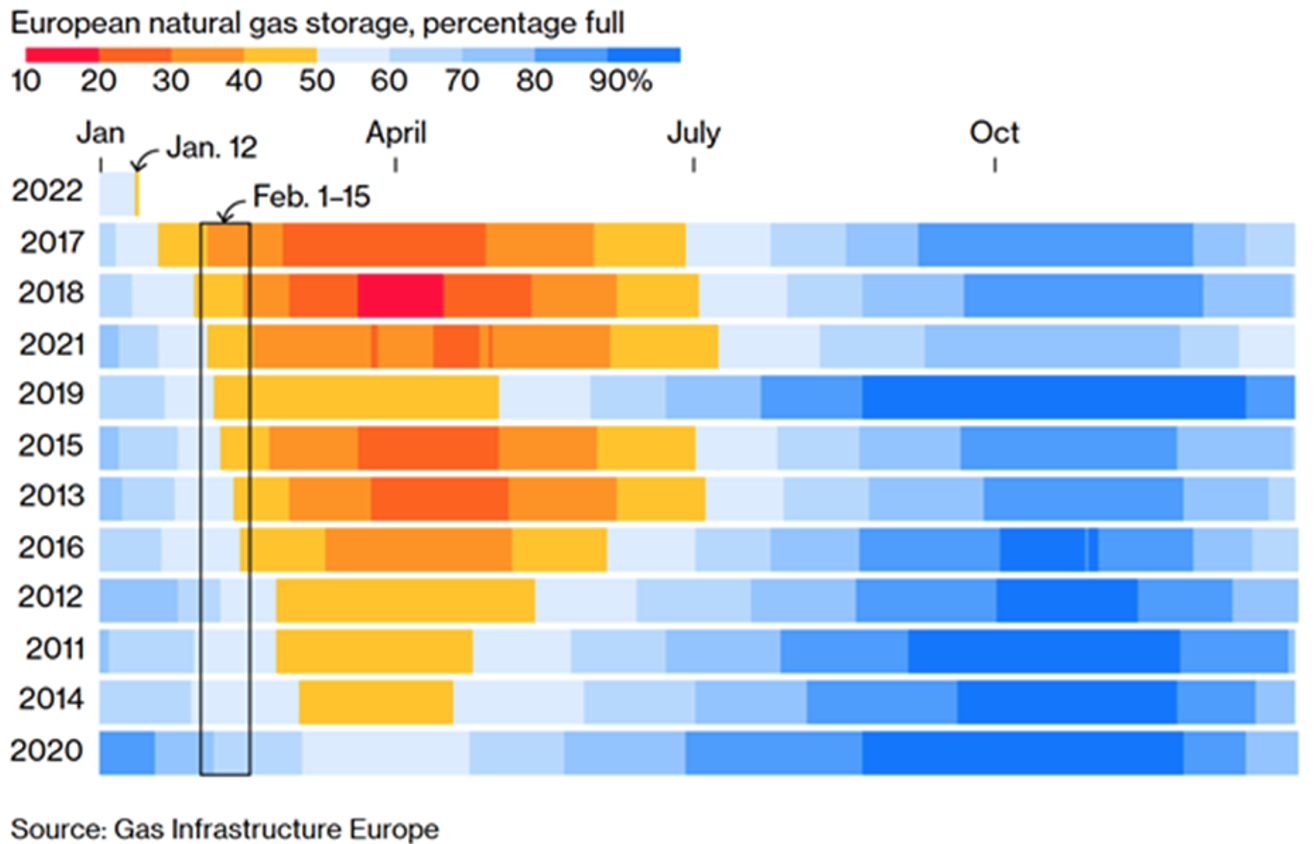

Looking at Europe’s storage inventories, constraints on physical import volumes driven in part by high wholesale Gas and LNG prices have resulted in inventories reaching their lower limits sooner than ever. The image below shows that European gas storage inventories in 2022 have fallen below the 50 per cent full mark sooner in the year than any of the past 11 years .

With Russian tensions high, gas price rises on the European markets – compounded by dwindling inventories – have the potential to reroute UK-bound exports from Norway toward the EU, unless the UK trading hub (the NBP) quickly corrects to replicate the rising prices in continental Europe.

The climate impact of precarious energy policy

Not only does this arrangement expose the UK to extreme price volatility, but it also means that the only float the UK has available to meet instances of variable demand, domestic supply decline, or changes in volumes supplied by Norway, is through LNG imports purchased on the spot markets.

This is where the first climate-relevant metric should be considered in the context of Cambo, Rosebank and Glendronach: domestically produced gas would have an average carbon intensity of around 22 kgCO2/boe, compared to the average LNG import, which has a carbon intensity of 59 kgCO2/boe – almost three times higher. That’s the average, and doesn’t account for the increasingly extreme events that we see on the volatile global LNG trading markets.

One such event that acts to highlight the potential climate issues of relying on LNG as the supply float, is the story of the LNG tanker Hellas Diana. The vessel loaded its cargo from Corpus Christi in November 2021, entering the Panama Canal in December. It travelled half-way across the pacific before market forces became so extreme that the most profitable option was to turn around, pay another set of Panama Canal fees, and incur huge fuel and cargo boil-off costs as it steamed thousands of miles to deliver its cargo to the UK in January this year. And yes, the consumer pays for this.

Risks to meeting UK demand

The largest ongoing risk to the UK’s pipeline imports from Norway (and LNG imports in a different way) is the geopolitical tensions between Russia and Europe in relation to the situation with Ukraine.

Russia supplies 35 per cent of Europe’s gas, and any escalation in the situation with Ukraine could see either physical disruption of supply, or more likely, a sanction and counter-sanction scenario.

Since Brexit, the UK is no longer a part of the 2017 EU Security of Supply Regulation, which was designed to safeguard supply through maintaining a functioning internal European energy market. Whilst the new UK-EU trade and cooperation agreement does make reference to cooperation through crises, the agreement prioritises maintaining market forces over direct intervention. As it stands, there is no compulsory agreement between the UK and the EU.

Whilst Norway is not an EU member state, it is a member of the EEA. As the second largest natural gas supplier to Europe after Russia, there is a conceivable risk that Norway will be required to direct more of its physical production toward Europe (and by extension, less to the UK), if Russian counter-sanctions threaten a European energy market meltdown.

This could lock the UK into further reliance on extremely costly LNG imports (both for the climate and for the economy), and could remain as such for the period of years it will take us to transition the 85 per cent of our housing fuel sources, and the arguably more straightforward 40 per cent of our electricity mix.

Developing UK domestic supply

There are only two available mitigations for a run-away energy price and emissions scenario over the next few years as we work as quickly as possible to manage the transition of our domestic heating and electricity mix away from hydrocarbons: more domestic gas production (and therefore less imports), and more domestic gas storage.

The higher that our domestically produced gas is as a percentage of our overall consumption, the lower our climate impact will be while we transform the underlying energy systems. The more gas storage capacity we have, the less susceptible we’ll be to market volatility.

For this reason, it’s not enough to simply look at projects like Cambo, Rosebank and Glendronach and suggest that we’ll be a greener nation by not developing them; the whole system needs to be assessed in order to understand that the default alternatives (mainly LNG) which will automatically fill the gaps created in supply through lack of domestic production are significantly more damaging to the environment and the economy than the development itself.

The part that is difficult about this is that it’s clearly a sub-optimal choice. We absolutely should be moving as quickly as we can away from hydrocarbons and towards new, less-damaging alternatives.

But to do as little harm as possible in the process, we need to focus on the demand side of the equation, not the supply side. Short of causing total societal collapse by halting hydrocarbon use overnight, we will be required to make complex choices along the way that at times may feel counterintuitive to the clear simplicity of our collective destination.